Can Circle's IPO Sprint to a $5 Billion Valuation Rewrite the Stablecoin Race Track?

On March 31, 2025, the cryptocurrency industry welcomed a significant piece of news. According to Fortune magazine's report, the issuer of the US dollar stablecoin USDC, Circle, is actively pushing forward with its IPO plan. Circle has now engaged JPMorgan Chase and Citigroup as underwriters and is expected to formally submit its public offering filing by the end of April, with a targeted valuation between $4 billion and $5 billion. This has drawn market attention to the recent hot stablecoin race.

Circle IPO Resurfaces

Interestingly, this is not Circle's first IPO plan. Back in 2018, Circle had already shown interest in the public market. At that time, Circle, through the acquisition of the cryptocurrency exchange Poloniex and the launch of USDC, quickly gained prominence. In the same year, Circle announced a $110 million funding round led by Bitmain, with IDG Capital, Breyer Capital, and other existing shareholders participating, valuing the company at $3 billion. This funding round may have signaled Circle's path to a future IPO, but the harsh bear market in the cryptocurrency space and a 75% valuation drop for Circle in early 2019 delayed the IPO plan.

What truly brought Circle close to the public market was the 2021 SPAC (Special Purpose Acquisition Company) craze. In July 2021, Circle announced a merger with the SPAC Concord Acquisition Corp. However, Circle soon faced regulatory challenges. The U.S. SEC increased scrutiny on SPAC transactions, demanding stricter financial disclosures and compliance measures. In December 2022, the Circle and Concord transaction fell through as it failed to receive SEC approval, and the company publicly stated it "terminated the SPAC plan." Over the next three years, Circle focused on enhancing USDC's compliance and market penetration, such as partnering with Visa to expand payment scenarios and applying for regulatory licenses worldwide.

Related Reading: "Retrospect on Circle: Fundraising with Bitcoin's Story and Listing with a Stablecoin's Story"

To understand Circle's IPO plan, one must mention its partner Coinbase's successful experience. On April 14, 2021, Coinbase went public on NASDAQ, becoming the first major cryptocurrency exchange to do so in the U.S. The opening price surged from $250 to $328.28, reaching an intraday high of $429, and the market cap soared to $64.5 billion. Coinbase CEO Brian Armstrong has expressed his hope for USDC to become the "world's largest stablecoin." If Circle's IPO succeeds, it will not only inject funds and resources into this goal but also potentially further solidify the strategic alliance between the two companies.

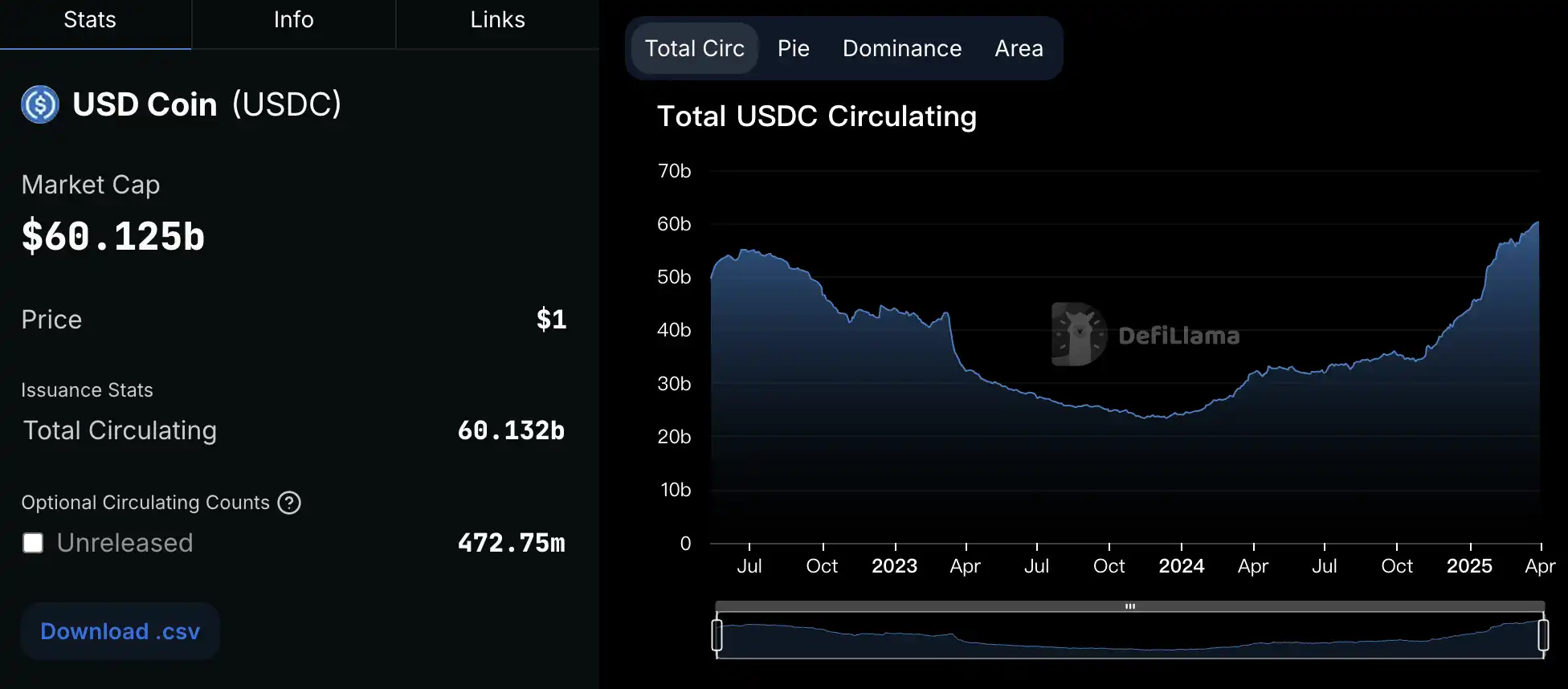

The relationship between Coinbase and Circle is more than just a regular partnership. In 2018, the two companies jointly launched USDC. As Circle's core product, the issuance and management of USDC rely heavily on Coinbase's support, and Coinbase also vigorously promotes USDC through its platform. By 2025, the market capitalization of USDC has exceeded 60 billion US dollars, making it the second largest stablecoin after Tether (USDT). Coinbase not only supports Circle in technology and marketing but also holds a portion of Circle's equity. This close collaboration has added more excitement to Circle's IPO.

Related Read: "A Conversation with Circle's Founder: Reflections on Circle's Turbulent Decade"

Circle vs. Tether: Fierce Rivals in the Stablecoin Race

In the stablecoin market, Circle's USDC and Tether's USDT see each other as top competitors. With a market capitalization of around 140 billion US dollars, USDT holds the throne, while USDC closely follows with 60 billion US dollars. Although there is still a gap between the two in market share, Circle is gradually narrowing the distance with Tether through its compliance and transparency.

Since its launch in 2014, Tether has become the dominant force in the stablecoin market due to its first-mover advantage and wide range of use cases. However, Tether's rise has not been without controversy. The transparency of its reserve assets has always been a focus of concern for regulatory agencies and investors. Although Tether claims that its USDT is fully backed 1:1 by the US dollar or other equivalent assets, the lack of multiple audit reports and doubts about its reserves have led to criticism.

In contrast, Circle is a leader in compliance. Each USDC token is backed by audited US dollar reserves, and Circle regularly publishes proof reports from top accounting firms. This transparency has not only earned favor from traditional financial institutions but also made it a "model student" in the eyes of regulators. For example, Circle has obtained money transmission licenses in multiple states in the United States and chose France as its headquarters in Europe to expand its global presence. In 2024, Circle also received regulatory approval in Japan to launch USDC, further expanding its international influence.

Related Read: "WSJ: The Life and Death Struggle of Tether and Circle"

The profit logic of stablecoins is not complicated. Taking Tether as an example, when users exchange dollars for USDT, Tether invests these funds in low-risk assets such as U.S. Treasury bonds and money market funds, earning interest differentials while maintaining the 1:1 peg with the dollar. During the high-interest rate cycle from 2022 to 2024, the U.S. Treasury bond yield exceeded 5% at one point, bringing substantial returns to Tether. Additionally, Tether further increases its revenue by charging withdrawal fees and sharing profits with partners. Tether achieved a full-year profit of up to $13 billion in 2024, a figure that even surpassed the annual revenue of BlackRock, the world's largest asset management company. This business model has almost no costs but can generate continuous cash flow, making it a "money printer of the digital age."

Circle's USDC follows a similar profit model, but due to its smaller market size, its revenue naturally lags behind Tether. However, Circle's transparency and compliance have won it more institutional customers. For example, Visa and Mastercard have integrated USDC into their payment networks, and BlackRock also indirectly supports USDC applications through its BUIDL fund. If Circle's IPO can successfully raise billions of dollars, it may accelerate its expansion in the institutional market and narrow the revenue gap with Tether.

Stablecoin Legislation Fuels the Fire

Circle's decision to push for an IPO this year is inseparable from the improvement in the external environment. Since Trump's election, he has publicly supported cryptocurrency development multiple times, promising to make the U.S. a "global crypto center" and emphasizing the dominance of the dollar in the digital economy. As a vital carrier of the digitization of the dollar, stablecoins naturally became a policy focus.

As of April 1, 2025, the U.S. legislative process regarding stablecoins has accelerated, with the "GENIUS Act" and "STABLE Act" drawing significant attention. The "GENIUS Act," proposed in 2024, requires stablecoin issuers to have 100% of their reserve assets backed by cash or cash equivalents and subject to regular audits. It was voted through the Senate Banking Committee on March 13 this year with 18 votes in favor and 6 against, and is set to proceed to the full Senate for a vote, with Bo Hines, Executive Director of the Presidential Digital Assets Advisory Committee, expecting to submit it for Trump's signature by June at the earliest. Meanwhile, the "STABLE Act" is steadily progressing in the House of Representatives, with plans for markup revisions on April 2. Currently, both chambers are coordinating the details of the bill, with explicit support from the Trump administration, pledging swift enactment into law once passed. This development provides policy advantages for compliance-focused stablecoin companies like Circle and signifies a clearer regulatory framework for the digital dollar in the U.S.

Further Reading: "Why Did $900 Billion Evaporate from the Crypto Market While Stablecoin Market Cap Hit a New High?"

In addition, the EU's "Markets in Crypto-Assets" (MiCA) regulation is set to be fully implemented in 2024, imposing greater transparency and capital requirements on stablecoin issuers. Circle has taken the lead by establishing its European headquarters in France, demonstrating its commitment to global compliance. Countries like Japan and the UK are also accelerating the development of stablecoin regulatory policies, providing clearer guidance for industry growth.

The enactment of stablecoin legislation may have a profound impact on the market landscape. For Circle, the success of its IPO could not only provide funding support but also drive greater adoption of USDC in regulated markets. In contrast, Tether faces increased regulatory pressure, requiring adjustments to its reserve structure, possibly including the sale of some non-cash assets. It is foreseeable that with a clearer regulatory environment and institutional funds entering the scene, the stablecoin market may undergo a reshuffle, with Circle's IPO potentially serving as a significant catalyst in this process.

Rise in Cryptocurrency IPO Activity

Against the backdrop of increasingly clear stablecoin regulations, Circle's IPO plan may just be a microcosm of traditional capital entering the crypto market. The policy tailwind has not only paved the way for stablecoin issuers like Circle but also opened the door to Wall Street for more crypto companies. Bitwise predicted at the end of last year that five companies (including Circle) could go public by 2025:

· Circle: Issuer of the second-largest stablecoin, USDC.

· Figure: Known for blockchain-based financial services such as mortgage and personal loans, and asset tokenization, the company has been exploring going public since last year.

· Kraken: The US-based cryptocurrency exchange has had IPO plans dating back to 2021.

· Anchorage Digital: Its status as a federally chartered bank may pave the way for its listing.

· Chainalysis: A leader in blockchain compliance and intelligence services, poised for listing.

Moreover, Hadick from Dragonfly stated: "I expect the LP (Limited Partner) market to get better, and they will want to put more capital into crypto. Many traditional Web2 crossover funds will return to Web3. We are already seeing this trend in some areas, such as stablecoins and payments." He added that venture capital transactions often lag behind public market price increases by a quarter or two.

Related Read: "Forbes: Cryptocurrency Will Be Redefined by 2025"

Circle's IPO may also become a milestone for the stablecoin industry's development. With the gradual clarification of the global regulatory environment, stablecoins are entering a golden age of compliance and institutionalization. Can Circle take advantage of this opportunity to further challenge Tether's dominant position? The answer will be revealed in the market performance after the IPO.

You may also like

Perp DEX: The Next Generation Exchange "War"

The AI gamble of mining companies: Valuations enter a phase of differentiation, and it's hard to turn the tide

A letter from Alliance to entrepreneurs: Written on the occasion of Cursor selling for 60 billion dollars

Stablecoins Finally Find Real Returns: On-Chain Reinsurance Re Explained | Interview with Re Founder Karan Saroya

The impossible triangle is simply a pseudo problem

Will MicroStrategy fall into a death spiral? What will the macro trend be in the second half of the year?

Blockchain Capital Partner: The Core Secret of Arbitrage

STRC unanchored by 11%, can the perpetual motion machine of Strategy still operate?

Bitcoin Market Analysis 2026: Can BTC Reach $150K by Year-End?

Bitcoin ETF Outflows Hit a Record $4.4 Billion: What Are Traders Doing With Their Cash?

WEEX App Just Got Smarter – New Tabs for Faster Trades & Easy Asset Management

WEEX All-New Search Features: Find, Trade & Earn Faster Than Ever

Morning Report | Illinois signs the strictest digital asset tax law in the U.S.; RWA tokenization market size surpasses $43 billion, institutions accelerate the migration of on-chain assets

Full version of the debut Q&A! Federal Reserve Chairman Waller: Sticking to the 2% inflation target, establishing five special working groups, individual did not submit the dot plot

From Disruptor to Shadow Market: The Crypto Market is Becoming a Colony of Traditional Finance

Dalio's important long article: How to position in the current market environment?

OKX Star analyzes Binance's competitive advantages: when regulation levels the playing field, competition has just begun