Coinbase Launches Binance Alpha2.0 Competitor, While Base Leading DEX Suffers Betrayal

Yesterday, Binance just updated Binance Alpha2.0, allowing CEX users to purchase any DEX token directly from CEX without the need for withdrawal. CZ also commented, "I believe other CEXs will follow suit, and DEX trading volume will also increase." Following closely, Coinbase made its move.

Last night, Coinbase announced the launch of Verified Pools, a set of carefully curated liquidity pools. Users holding Coinbase Verifications certification can seamlessly conduct on-chain transactions by connecting their Prime Onchain wallet, Coinbase wallet, or other third-party wallets to Coinbase Verification credential for trading. This aims to address the opacity issue in traditional liquidity pools.

Verified Pools on the Base network are based on the Uniswap v4 protocol, leveraging a hooks mechanism to enable customizable smart contract functionality. Additionally, it has partnered with DeFi research and risk management firm Gauntlet to optimize liquidity pool configurations and ensure the overall health of the liquidity pools.

In the official announcement, Verified Pools are described as another important step by Coinbase to drive the adoption of on-chain applications. However, what surprised users in the Base community the most was that Verified Pools are based on Uniswap V4 instead of Aerodrome, Base's largest on-chain DEX application. Some even referred to this behavior as a "betrayal" of Aerodrome.

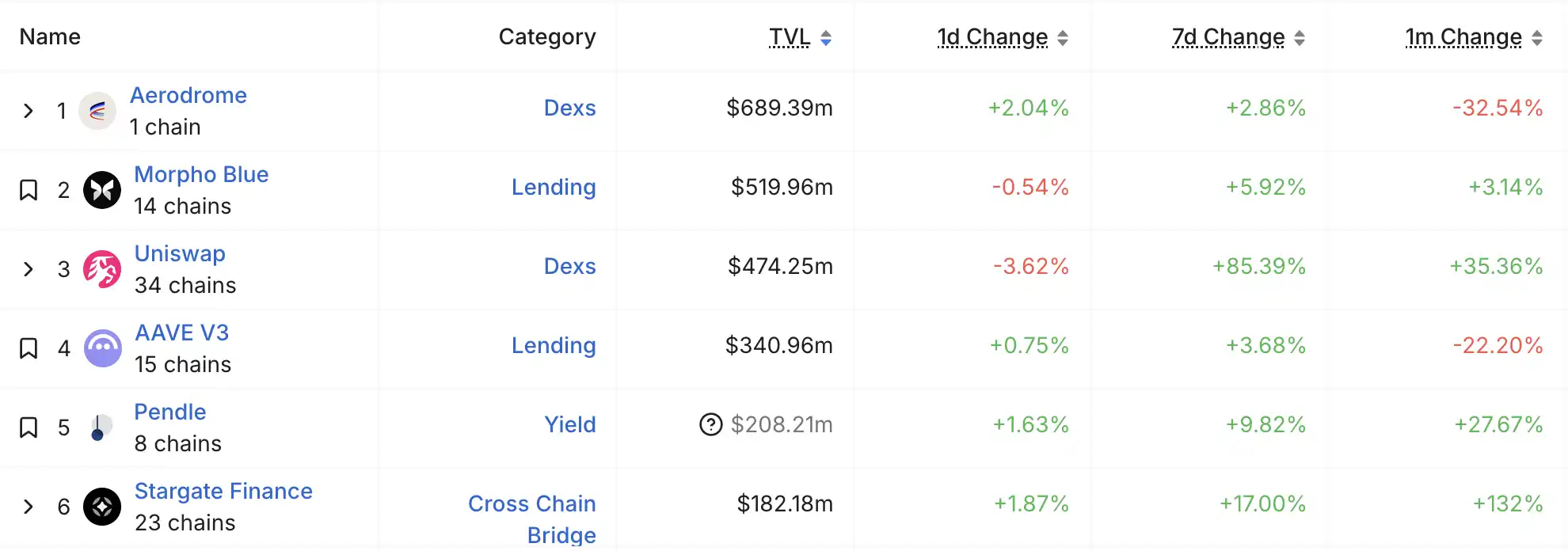

Aerodrome is ranked first in TVL on Base; Image Source: DeFiLlama

So why did Coinbase's Verified Pools choose Uniswap instead of Aerodrome?

Compliance First, Uniswap is a More Cost-Effective Choice

There are many who do not understand Coinbase's approach, with even Sonic founder Andre Cronje asking, "Really confusing, Aerodrome and Alex have always been Base's most staunch supporters and advocates, this could have been completely built on Aerodrome. Isn't supporting your builders a slogan?"

In response to these questions, Aerodrome co-founder Alexander Cutler stated, "We had conversations with them early in our development and were fully capable of adding the same functionality—it just wasn't a priority at the time, but we will definitely watch its adoption."

He mentioned that Coinbase reached out to Aerodrome for a collaboration on a validation pool last summer, but there were still many unresolved issues with the validation pool's Product-Market Fit (PMF), so Aerodrome chose a larger opportunity as a priority at that time.

The core of the Coinbase validation pool lies in its on-chain Credential system tied to KYC verification. Uniswap V4's hooks mechanism can be customized to only allow LPs verified through Coinbase's KYC to participate, and this technological feature directly addresses regulatory compliance issues.

Uniswap V4's hooks are essentially a smart contract "plugin system" that allows developers to customize pool creation rules, fee structures, and permission management. This flexibility enables Coinbase to quickly deploy a whitelist access mechanism that complies with its regulatory framework and achieves a strong binding of LP identities through the on-chain Credential system.

Read more: "When Binance Launchpool Meets Uniswap V4, Whose Ace Is Bigger?"

As Aerodrome, being the native DEX on the Base chain, is positioned as a "liquidity hub," its underlying codebase does not natively support such complex permission layering designs. Even if achieved through forking or refactoring in the future, the development cycle and testing costs would be significantly higher than directly adopting Uniswap's mature solution.

As a publicly listed company, Coinbase has a very low tolerance for compliance risks. Although Aerodrome is the native DEX on the Base chain, its permissionless and highly autonomous protocol features are fundamentally at odds with Coinbase's regulatory framework. By directly integrating Aerodrome, Coinbase would assume liability for protocol vulnerabilities, money laundering risks, and even regulatory scrutiny. In contrast, Uniswap V4's modular design allows Coinbase to gradually test the waters through a controlled KYC Isolation Pool, avoiding regulatory minefields while leveraging Uniswap's brand credibility and liquidity network.

Alexander Cutler also acknowledged the "technically feasible" aspect but explicitly stated that features such as dynamic fee rate optimization would be prioritized over permissioned pool functionality.

In response to someone else's tweet, he wrote, "There are still many questions about how permissioned pools can become attractive enough to serve as a viable alternative to permissionless pools. If it truly gains market acceptance, we can always join in support. However, in the short term, it's unlikely to surpass opportunities like dynamic fees."

This choice reflects Aerodrome's inclination towards serving existing DeFi-native users rather than catering to Coinbase's compliance experiment. On the other hand, Coinbase aims to explore on-chain compliant transaction scenarios through the validation pool and gradually migrate CEX users to the chain, requiring instant usability and low compliance risk, with Uniswap V4 conveniently offering a ready-made technical interface.

More Experimental Than Product-Market Fit

However, some view whitelist liquidity pools as one of the anticipated use cases for Uniswap V4, with Coinbase's validation pool being merely the practical implementation of this concept. The most direct contradiction lies in the highly overlapping target users—institutional LPs on Coinbase's order book and compliant buyers are already accustomed to the low-friction environment of centralized trading platforms.

If on-chain centralized liquidity merely replicates CEX's order book functionality, users lack migration incentives—the gas costs, price slippage, and operational complexity of on-chain trading still exceed those of CEX, and traditional users rely more on CEX for instant settlement, fiat channels, and customer support. Even if the validation pool can offer slightly higher market-making returns, liquidity fragmentation may reduce capital efficiency, creating a dilemma of "compliance premium insufficient to cover migration costs."

A deeper challenge comes from the liquidity allocation paradox. If the validation pool focuses on Coinbase's unlisted assets, it will fall into a "chicken and egg" cycle: the high-risk nature of unaudited assets inherently conflicts with the conservative positioning of the compliance pool, and fund managers seeking alpha often lean towards early-stage assets on permissionless pools. This could turn the validation pool into a "compliance buffer zone" for market makers—earning fees through liquidity provision instead of capturing asset appreciation dividends.

Even if unlisted assets are allowed into the pool, whether they can serve as an "onboarding transition channel" remains questionable. As a publicly traded company, Coinbase will not relax its strict asset review standards due to the existence of on-chain pools; instead, it may tighten them further due to compliance pressure.

Despite Coinbase binding KYC identities on-chain, ZachXBT once revealed a systemic vulnerability: The dark web can exploit a risk of injecting illicit funds by purchasing/stealing KYC information to forge a "compliant identity." If a hacker offloads illegal ETH to a validation pool through a market maker, the disparity between on-chain anonymity and CEX risk management capabilities may lead to the entire pool being flagged as a "tainted asset pool," triggering regulatory scrutiny. More subtly, arbitrage bots still need to rely on market makers to balance prices, but the risk management capabilities of market makers are far below those of centralized CEX systems, ultimately potentially shifting the risk to ordinary users.

In the short term, the validation pool appears more like an "on-chain feasibility study"—utilizing Uniswap V4's hooks mechanism to build a minimal compliance model, testing regulatory tolerance and user behavior data; in the medium term, the plan is to iterate the interactive interface developed for this into an on-chain transaction standard tool, paving the way for future permissionless pool integration; the long-term goal remains to blur the boundaries between CEX and DEX, gradually realizing Brian Armstrong's vision of "on-chain/off-chain liquidity unification."

However, whether this experiment can overcome the "sandbox-to-reality" gap depends on two key variables: first, whether the U.S. SEC will view such pools as a "quasi-securities trading platform," and second, whether the speed of CEX user migration to on-chain can support liquidity density. At this stage, it is still too early to assert its success or failure.

You may also like

The AI gamble of mining companies: Valuations enter a phase of differentiation, and it's hard to turn the tide

A letter from Alliance to entrepreneurs: Written on the occasion of Cursor selling for 60 billion dollars

Will MicroStrategy fall into a death spiral? What will the macro trend be in the second half of the year?

Blockchain Capital Partner: The Core Secret of Arbitrage

STRC unanchored by 11%, can the perpetual motion machine of Strategy still operate?

Bitcoin Market Analysis 2026: Can BTC Reach $150K by Year-End?

Bitcoin ETF Outflows Hit a Record $4.4 Billion: What Are Traders Doing With Their Cash?

WEEX App Just Got Smarter – New Tabs for Faster Trades & Easy Asset Management

WEEX All-New Search Features: Find, Trade & Earn Faster Than Ever

Morning Report | Illinois signs the strictest digital asset tax law in the U.S.; RWA tokenization market size surpasses $43 billion, institutions accelerate the migration of on-chain assets

Full version of the debut Q&A! Federal Reserve Chairman Waller: Sticking to the 2% inflation target, establishing five special working groups, individual did not submit the dot plot

From Disruptor to Shadow Market: The Crypto Market is Becoming a Colony of Traditional Finance

Dalio's important long article: How to position in the current market environment?

OKX Star analyzes Binance's competitive advantages: when regulation levels the playing field, competition has just begun

New gameplay for participating in initial offerings on cryptocurrency exchanges

Why Is Bitcoin Down Today? What the Hawkish FOMC Means for SpaceX, Gold and Nasdaq

DeepSeek Financing Story