- Buy Crypto

- Markets

Futures

Futures- Spot

- Copy Trade

Earn

Earn- More

Multicoin: Why Are We Bullish on Stablecoins as FinTech 4.0?

Original Title: Specialized Stablecoin Fintechs

Original Authors: Spencer Applebaum, Eli Qian, Multicoin Capital

Original Translation: Techflow of DeepTech

Over the past two decades, financial technology (fintech) has transformed how people access financial products, but has not fundamentally changed the way money moves.

Innovation has largely focused on cleaner interfaces, smoother user experiences, and more efficient distribution channels, while the core financial infrastructure has remained largely unchanged.

For much of this time, the fintech stack has been more about reselling rather than rebuilding.

Overall, the evolution of fintech can be divided into four stages:

FinTech 1.0: Digital Distribution (2000-2010)

The earliest wave of fintech made financial services more accessible but did not significantly improve efficiency. Companies like PayPal, E*TRADE, and Mint digitized existing financial products by combining traditional systems (such as decades-old ACH, SWIFT, and card networks) with internet interfaces.

During this phase, fund settlement was slow, compliance processes were reliant on manual operations, and payment processing was constrained by strict timelines. Although this period brought financial services online, it did not fundamentally change the way money moves. What changed was only who could use these financial products, not how these products actually operated.

FinTech 2.0: Neobank Era (2010-2020)

The next breakthrough came from the widespread adoption of smartphones and social distribution. Chime offered wage advance services to gig workers; SoFi focused on student loan refinancing for high-potential graduates; Revolut and Nubank, through user-friendly interfaces, served populations globally with limited financial service coverage.

While each company told a more appealing story to a specific audience, they were essentially selling the same product: checking accounts and debit cards running on the existing payment rails. They still relied on sponsor banks, card networks, and the ACH system, no different from their predecessors.

The reason these companies have been successful is not because they built a new payment network, but because they better reached the customer. Branding, user guidance, and customer acquisition became their competitive advantage. At this stage, fintech companies became enterprises mastering distribution attached to banks.

FinTech 3.0: Embedded Finance (2020-2024)

Around 2020, embedded finance rapidly emerged. The proliferation of APIs (Application Programming Interfaces) enabled almost any software company to offer financial products. Marqeta enables companies to issue cards through an API; Synapse, Unit, and Treasury Prime offer Banking-as-a-Service (BaaS). Soon, almost every application could offer payment, card, or lending services.

However, behind these abstraction layers, fundamentally, there has not been a radical change. BaaS providers still rely on early-stage sponsor banks, compliance frameworks, and payment networks. The abstraction layer shifted from banks to APIs, but economic benefits and control still revert to traditional systems.

Commoditization of FinTech

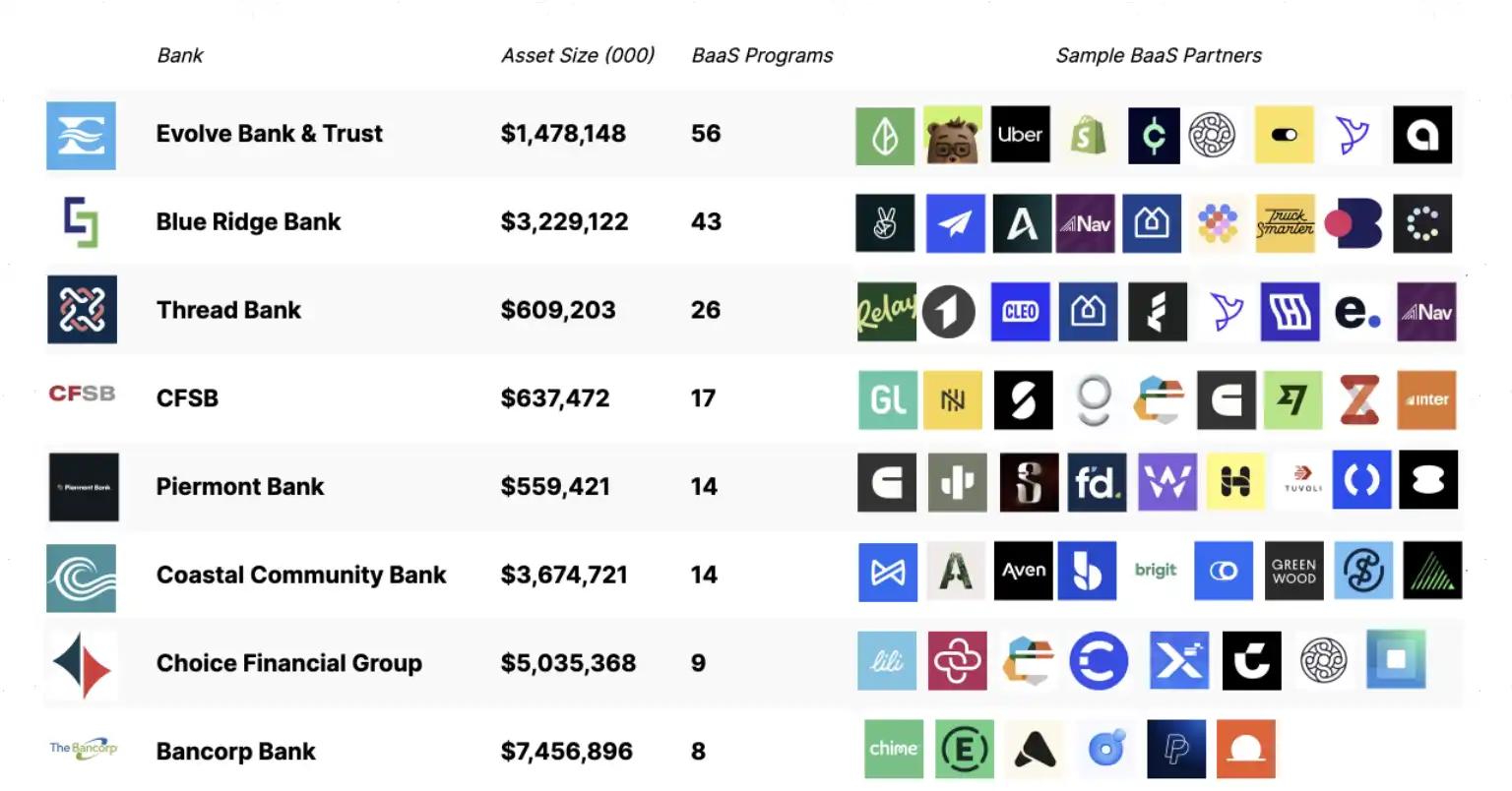

By the early 2020s, the flaws of this model began to emerge. Almost all major neobanks relied on the same small set of sponsor banks and BaaS providers.

Source: Embedded

As companies engaged in fierce competition through performance marketing, customer acquisition costs skyrocketed, profit margins were compressed, fraud and compliance costs surged, and infrastructure became almost indistinguishable. Competition evolved into a marketing arms race. Many fintech companies tried to differentiate themselves through card colors, signup bonuses, and cashback gimmicks.

At the same time, control of risk and value concentrated at the banking level. Large institutions like JPMorgan Chase and Bank of America, regulated by the OCC, retained core privileges: accepting deposits, issuing loans, and accessing federal payment networks (such as ACH and Fedwire). Fintech companies like Chime, Revolut, and Affirm lacked these privileges and had to rely on licensed banks to provide these services. Banks profit through interest spreads and platform fees; fintech companies rely on interchange fees for revenue.

With the rapid increase in FinTech projects, regulatory bodies have been subjecting the sponsoring banks to increasingly rigorous scrutiny. Regulatory orders and heightened supervisory expectations have compelled banks to dedicate significant resources to compliance, risk management, and oversight of third-party projects. For example, Cross River Bank entered into a compliance order with the Federal Deposit Insurance Corporation (FDIC); Green Dot Bank faced enforcement action by the Federal Reserve; and the Federal Reserve issued a cease and desist order to Evolve Bank.

The banks' response to this has been to tighten customer onboarding processes, limit the number of supported projects, and slow down product iteration speed. What was once a supportive environment for innovation now requires greater scale to justify the cost of compliance. The growth of the FinTech industry has become slower, more expensive, and more inclined to launch general-purpose products for a broad user base rather than focusing on specific use cases.

From our perspective, the three main reasons why innovation has remained at the top layer of the tech stack for the past 20 years are as follows:

1. Monopoly and Closed Nature of Fund Movement Infrastructure: Visa, Mastercard, and the Federal Reserve's ACH network have left little room for competition.

2. Startups Require Significant Capital to Launch Finance-Centric Products: Developing a regulated banking app requires millions of dollars for compliance, fraud prevention, fund management, etc.

3. Regulations Restrict Direct Involvement: Only licensed entities can hold funds or move funds through core payment networks.

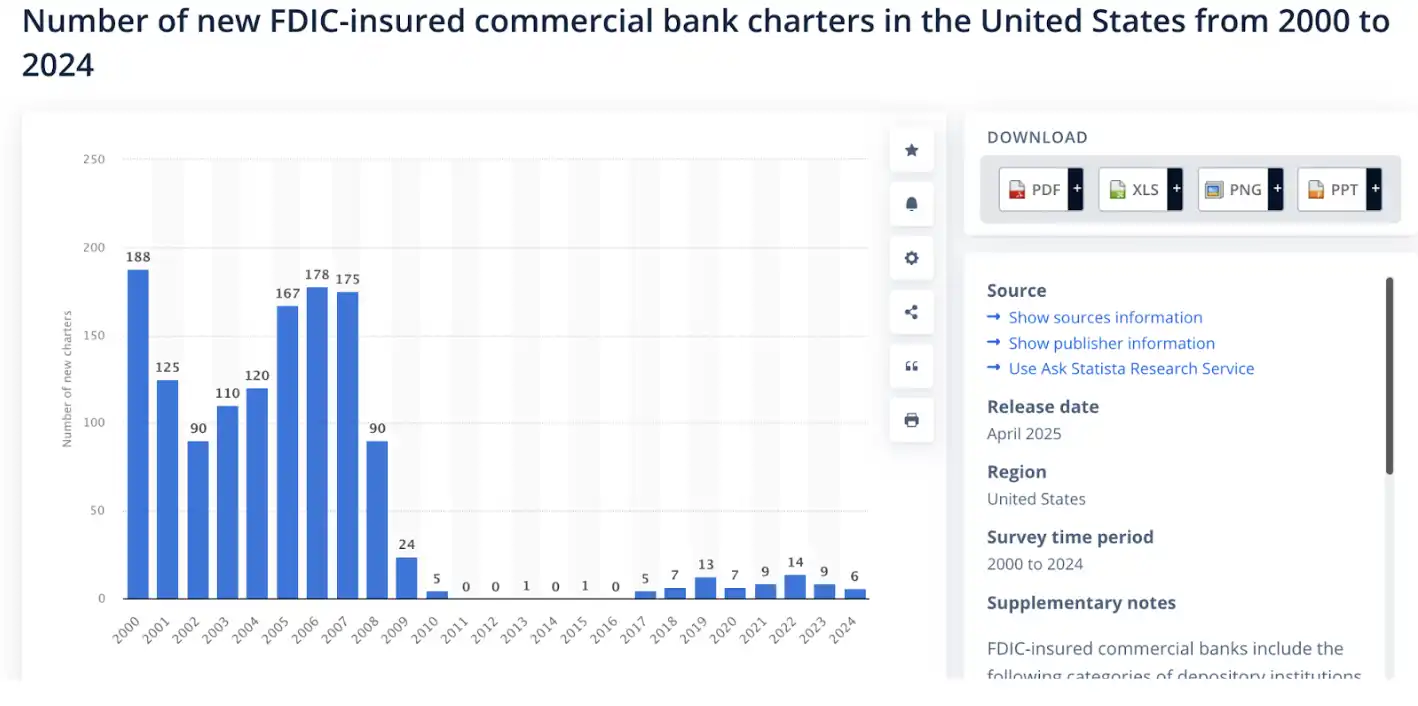

Source: Statista

Given these constraints, rather than directly challenging existing payment networks, it is wiser to focus on building products. As a result, most FinTech companies have essentially become slick wrappers around bank APIs. Despite numerous innovations emerging in the FinTech sector over the past two decades, there have been few truly new financial primitives born in the industry. For a long time, there have been almost no practical alternative solutions.

The crypto industry, on the other hand, has taken a completely different path. Developers first focused on building financial primitives. From Automated Market Makers (AMMs), Bonding Curves, Perpetual Contracts, Liquidity Vaults to on-chain credit, all of these have gradually evolved from the foundational level. For the first time in history, financial logic itself has become programmable.

FinTech 4.0: Stablecoins and Permissionless Finance

While the first three eras of FinTech saw many innovations, the underlying funds transfer architecture remained largely unchanged. Whether financial products were delivered through traditional banks, neobanks, or embedded APIs, funds still flowed on a closed permissioned network controlled by intermediaries.

Stablecoins have disrupted this pattern. Rather than building software on top of banks, they have directly replaced core banking functions. Developers can interact directly with an open, programmable network. Payments settle on-chain, custody, lending, and compliance shift from traditional trust relationships to software-enforced rules.

While Banking as a Service (BaaS) reduced friction, it did not alter the economic model. FinTech companies still need to pay compliance fees to sponsoring banks, settlement fees to card networks, and access fees to intermediaries. The infrastructure remains costly and siloed.

Stablecoins, on the other hand, eliminate the need for rented access entirely. Developers no longer need to call bank APIs but can interact directly with an open network. Settlements occur directly on-chain, with fees flowing to the protocol rather than intermediaries. This shift is believed to significantly lower the cost barrier—from needing millions of dollars to develop through a bank, or tens of thousands through BaaS, to just thousands of dollars through permissionless on-chain smart contracts.

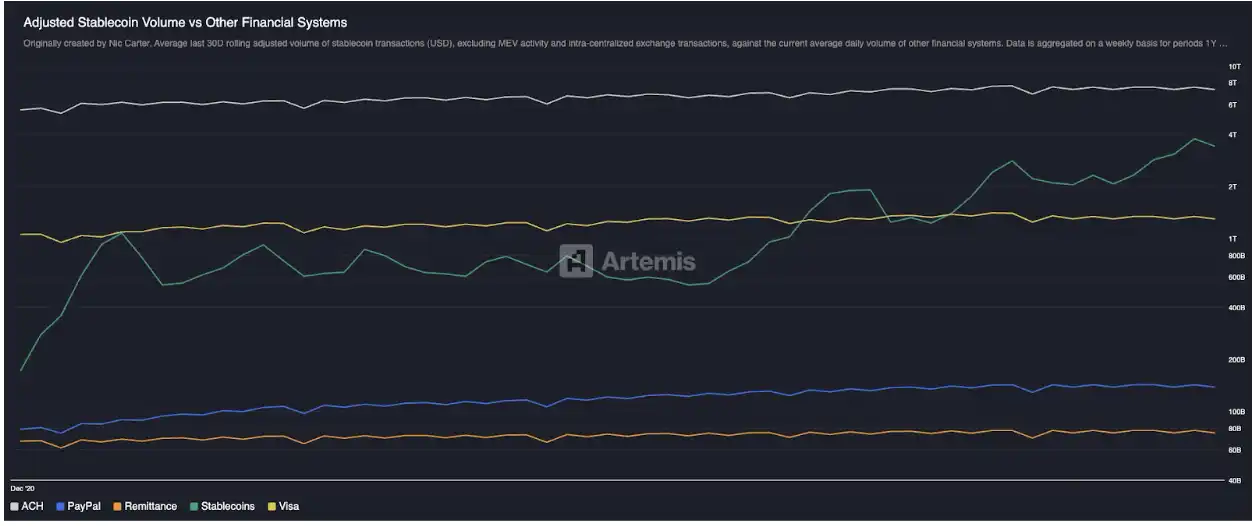

This shift has already manifested in large-scale applications. The stablecoin market cap has grown from nearly zero to around $300 billion in less than a decade, even excluding transfers between trading platforms and Miner Extractable Value (MEV). The actual economic transaction volume it processes has surpassed traditional payment networks like PayPal and Visa. For the first time, a non-bank, non-card payment network has been able to truly achieve global scale operation.

Source: Artemis

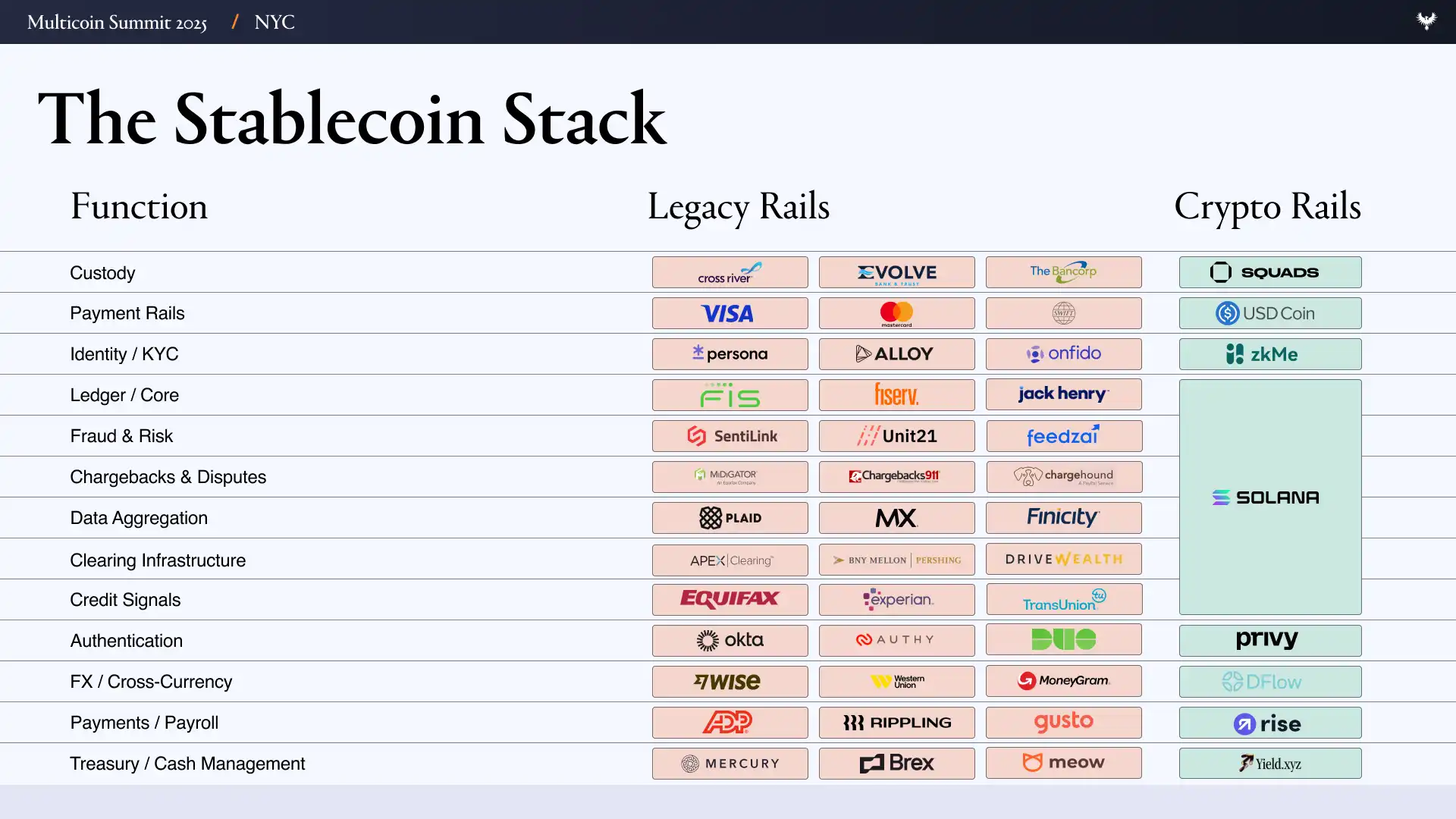

To understand the significance of this shift in practice, we must first comprehend how FinTech is currently built. A typical FinTech company relies on an extensive vendor tech stack, including the following layers:

· User Interface/User Experience (UI/UX)

· Banking and Custody Layer: Evolve, Cross River, Synapse, Treasury Prime

· Payment Networks: ACH, Wire, SWIFT, Visa, Mastercard

· Identity & Compliance: Ally, Persona, Sardine

· Fraud Prevention: SentiLink, Socure, Feedzai

· Underwriting/Credit Infrastructure: Plaid, Argyle, Pinwheel

· Risk & Treasury Infrastructure: Alloy, Unit21

· Capital Markets: Prime Trust, DriveWealth

· Data Aggregation: Plaid, MX

· Compliance/Reporting: FinCEN, OFAC Checks

Launching a fintech company on this tech stack means managing dozens of partner contracts, audits, incentive mechanisms, and potential failure modes. Each layer adds cost and latency, and much of the team's time is spent coordinating infrastructure rather than focusing on product development.

On the other hand, a stablecoin-based system dramatically simplifies this complexity. What used to require multiple vendors can now be achieved through a few on-chain primitives.

In a world centered around stablecoins and permissionless finance, the following changes are taking place:

· Banking and Custody: Replaced by decentralized solutions like Altitude.

· Payment Networks: Replaced by stablecoins.

· Identity & Compliance: Still necessary, but we believe this can be achieved on-chain and maintained through technologies like zkMe for confidentiality and security.

· Underwriting and Credit Infrastructure: Completely revamped and moved on-chain.

· Capital Markets Firm: These types of companies will become irrelevant when all assets are tokenized.

· Data Aggregation: Replaced by on-chain data and selective transparency (e.g., via Fully Homomorphic Encryption FHE).

· Compliance and OFAC Checks: Handled at the wallet level (e.g., if Alice's wallet is on a sanctions list, she will not be able to interact with the protocol).

The true differentiator of FinTech 4.0 is that the foundational infrastructure of finance is finally beginning to change. Instead of building an application that needs to quietly ask banks for permission in the background, people now interact directly with stablecoins and open payment networks, replacing core banking functions. Developers are no longer tenants but have become true owners of the "land."

The Opportunity for Stablecoin-Focused Fintech

The first-order impact of this shift is straightforward: the number of FinTech companies will increase dramatically. When custody, lending, and fund transfers become nearly free and instant, starting a FinTech company will be as simple as launching a SaaS product. In a stablecoin-centric world, there is no longer a need for complex integrations with sponsor banks, card issuance intermediaries, multi-day settlement processes, or redundant KYC (Know Your Customer) checks that slow down progress.

We believe that the fixed cost of creating a finance-centric FinTech product will plummet from millions of dollars to thousands. With infrastructure, customer acquisition costs (CAC), and compliance barriers disappearing, startups will be able to profitably serve smaller, more specific social groups through what we refer to as "Stablecoin-Focused Fintech" model.

This trend has a clear precedent in history. The last generation of FinTech companies initially gained traction by serving specific customer segments: SoFi focused on student loan refinancing, Chime offered early paycheck services, Greenlight targeted teens with debit cards, and Brex served entrepreneurs unable to access traditional business credit. However, this focused model did not become a sustainable operating model. Due to constrained transaction fee income, rising compliance costs, and reliance on sponsor banks, these companies were forced to expand beyond their original niche areas. To survive, teams were forced to horizontally scale, adding products that users didn't need just to scale infrastructure to maintain viability.

Today, thanks to the emergence of a crypto payments network and permissionless financial APIs that significantly lower the barrier to entry, a new wave of specialized neobanks will arise, each targeting specific user segments much like the early fintech innovators. With greatly reduced operational costs, these neobanks can focus on narrower, more specialized markets and maintain that focus, such as Sharia-compliant finance, cryptocurrency enthusiast lifestyle services, or offerings designed for athletes' unique income and spending patterns.

Of even greater impact, specialization can significantly enhance unit economics. Customer Acquisition Costs (CAC) decrease, cross-selling becomes easier, and Customer Lifetime Value (LTV) increases. Focused fintech companies can precisely target a niche group that can be efficiently converted, gain more word-of-mouth referrals through serving specific user segments, spend less on operations, and yet extract more revenue per customer compared to the previous generation of fintech companies.

As anyone can launch a fintech company within weeks, the question shifts from "Who can reach the customer?" to "Who truly understands the customer?"

Exploring the Design Space of Specialized Fintech

The most attractive opportunities often lie where traditional payment networks fail.

Take adult content creators and performers, for example, who generate billions of dollars in revenue annually but are often "deplatformed" by banks and card payment processors due to reputational risks or refund risks. Their income payments may be delayed by days or even withheld due to "compliance reviews" and typically require payment gateway fees of 10%-20% through high-risk gateways like Epoch, CCBill, etc. We believe that stablecoin-based payments can offer instant, irreversible settlement, support programmable compliance, enable performers to self-host income, automatically allocate income to tax accounts or savings, and receive payments globally without relying on high-risk intermediaries.

Look at professional athletes next, especially individual sport athletes like golfers and tennis players, who face unique cash flow and risk dynamics. Their income is concentrated within a short professional career lifespan, often needing to be shared with agents, coaches, and team members. They need to pay taxes in multiple states and countries, and an injury could completely halt their income source. A stablecoin-based fintech company can help them tokenize future earnings, pay team wages using a multi-signature wallet, and automatically withhold taxes based on different regional tax requirements.

Luxury goods and watch dealers are another category of market poorly served by traditional financial infrastructure. These businesses often transfer high-value inventory across borders, typically completing six-figure transactions via wire transfer or high-risk payment processors, all while enduring multi-day settlement times. Their working capital is often locked up in inventory sitting in safes or display cases rather than bank accounts, making short-term financing both expensive and hard to come by. We believe a stablecoin-based fintech company could directly address these issues by providing instant settlement for large transactions, offering lines of credit collateralized by tokenized inventory, and delivering programmable custody services with built-in smart contracts.

As you examine a sufficient number of these use cases, you will find the same constraints recurring time and again: traditional banks have not catered to users with global, non-standard, or unconventional cash flows. Yet, these cohorts can become profitable markets through a stablecoin payment network. Here are some theoretical case examples of focused stablecoin fintech that we find attractive:

· Professional Athletes: Income concentrated in a brief career span; often need to travel and relocate; may need to file taxes in multiple jurisdictions; required to pay salaries to coaches, agents, trainers, etc.; may wish to hedge injury risks.

· Adult Performers and Creators: Excluded by banks and card payment processors; audience spread worldwide.

· Unicorn Company Employees: Cash-strapped, net worth tied up in illiquid equity; may face hefty taxes upon option exercise.

· On-Chain Developers: Net worth concentrated in highly volatile tokens; encounter fiat off-ramp and tax issues.

· Digital Nomads: Passportless banking services, automated forex; automated tax handling based on location; frequent travel and relocation.

· Prisoners: Difficult and expensive for family or friends to deposit funds through traditional channels; funds often delayed in reaching them.

· Sharia-Compliant Financial Services: Avoidance of interest-based transactions.

· Generation Z: Distrust traditional banking services; invest in a gamified manner; financial services with social features.

· Cross-Border SMEs (Small and Medium-sized Enterprises): High forex fees; slow settlements; frozen working capital.

· Cryptocurrency Enthusiast (Degens): Engages in high-risk speculative trading by paying with a credit card bill.

· International Aid: Aid funding is slow to flow, restricted by intermediaries, and low in transparency; severe fund loss occurs due to fees, corruption, and misallocation of resources.

· Tandas / Rotating Savings and Credit Associations: Provides cross-border savings services for globalized families; pools savings for returns; can establish income history on-chain for credit assessment.

· Luxury Goods Dealer (e.g., Watch Dealer): Working capital is locked up in inventory; requires short-term loans; engages in high-value cross-border transactions in bulk; often completes transactions through chat applications like WhatsApp and Telegram.

Summary

Over the past two decades, fintech innovation has largely focused on the distribution layer rather than infrastructure. Companies compete in brand marketing, user acquisition, and fee-based customer monetization, but funds themselves still move through the same closed payment networks. While this has expanded the reach of financial services, it has also led to homogenization, rising costs, and inescapable thin margins.

Stablecoins are poised to fundamentally reshape the economic model of financial products. By transforming functions like custody, settlement, credit, and compliance into open, programmable software, they significantly reduce the fixed costs of starting and operating a fintech company. Functionalities that previously required reliance on sponsor banks, card networks, and a vast vendor tech stack can now be built directly on-chain, greatly reducing the operational costs required.

As infrastructure becomes cheaper, niche specialization becomes possible. Fintech companies no longer need millions of users to turn a profit. Instead, they can focus on niche, well-defined communities whose needs are not effectively met by one-size-fits-all products. For example, communities of athletes, adult creators, K-pop fans, or luxury watch dealers, these communities already share common cultural backgrounds, trust foundations, and behavioral patterns, allowing products to naturally spread through word of mouth rather than relying on paid marketing.

Equally important, these communities often have similar cash flow patterns, risks, and financial decision-making. This consistency allows product design to be optimized around people's actual income, spending, and fund management behavior, rather than abstract user personas. The effectiveness of word-of-mouth spreads not only because of mutual acquaintance among users but also because the product truly fits the operational mode of that community.

If this vision were to become a reality, this economic transformation would be profound. As distribution becomes more community-aligned, Customer Acquisition Cost (CAC) will decrease; and with fewer intermediaries, profit margins will increase. Markets that once seemed too small or lacked economic viability will transform into enduring and profitable business models.

In such a world, the advantage of fintech will no longer rely on simple scale expansion and high marketing expenses but will instead shift toward a profound understanding of user backgrounds. The success of the next generation of fintech will not be in trying to serve everyone but in being able to provide tailored services to specific groups based on actual fund flows.

You may also like

Token Cannot Compound, Where Is the Real Investment Opportunity?

February 6th Market Key Intelligence, How Much Did You Miss?

China's Central Bank and Eight Other Departments' Latest Regulatory Focus: Key Attention to RWA Tokenized Asset Risk

Foreword: Today, the People's Bank of China's website published the "Notice of the People's Bank of China, National Development and Reform Commission, Ministry of Industry and Information Technology, Ministry of Public Security, State Administration for Market Regulation, China Banking and Insurance Regulatory Commission, China Securities Regulatory Commission, State Administration of Foreign Exchange on Further Preventing and Dealing with Risks Related to Virtual Currency and Others (Yinfa [2026] No. 42)", the latest regulatory requirements from the eight departments including the central bank, which are basically consistent with the regulatory requirements of recent years. The main focus of the regulation is on speculative activities such as virtual currency trading, exchanges, ICOs, overseas platform services, and this time, regulatory oversight of RWA has been added, explicitly prohibiting RWA tokenization, stablecoins (especially those pegged to the RMB). The following is the full text:

To the people's governments of all provinces, autonomous regions, and municipalities directly under the Central Government, the Xinjiang Production and Construction Corps:

Recently, there have been speculative activities related to virtual currency and Real-World Assets (RWA) tokenization, disrupting the economic and financial order and jeopardizing the property security of the people. In order to further prevent and address the risks related to virtual currency and Real-World Assets tokenization, effectively safeguard national security and social stability, in accordance with the "Law of the People's Republic of China on the People's Bank of China," "Law of the People's Republic of China on Commercial Banks," "Securities Law of the People's Republic of China," "Law of the People's Republic of China on Securities Investment Funds," "Law of the People's Republic of China on Futures and Derivatives," "Cybersecurity Law of the People's Republic of China," "Regulations of the People's Republic of China on the Administration of Renminbi," "Regulations on Prevention and Disposal of Illegal Fundraising," "Regulations of the People's Republic of China on Foreign Exchange Administration," "Telecommunications Regulations of the People's Republic of China," and other provisions, after reaching consensus with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, and with the approval of the State Council, the relevant matters are notified as follows:

(I) Virtual currency does not possess the legal status equivalent to fiat currency. Virtual currencies such as Bitcoin, Ether, Tether, etc., have the main characteristics of being issued by non-monetary authorities, using encryption technology and distributed ledger or similar technology, existing in digital form, etc. They do not have legal tender status, should not and cannot be circulated and used as currency in the market.

The business activities related to virtual currency are classified as illegal financial activities. The exchange of fiat currency and virtual currency within the territory, exchange of virtual currencies, acting as a central counterparty in buying and selling virtual currencies, providing information intermediary and pricing services for virtual currency transactions, token issuance financing, and trading of virtual currency-related financial products, etc., fall under illegal financial activities, such as suspected illegal issuance of token vouchers, unauthorized public issuance of securities, illegal operation of securities and futures business, illegal fundraising, etc., are strictly prohibited across the board and resolutely banned in accordance with the law. Overseas entities and individuals are not allowed to provide virtual currency-related services to domestic entities in any form.

A stablecoin pegged to a fiat currency indirectly fulfills some functions of the fiat currency in circulation. Without the consent of relevant authorities in accordance with the law and regulations, any domestic or foreign entity or individual is not allowed to issue a RMB-pegged stablecoin overseas.

(II)Tokenization of Real-World Assets refers to the use of encryption technology and distributed ledger or similar technologies to transform ownership rights, income rights, etc., of assets into tokens (tokens) or other interests or bond certificates with token (token) characteristics, and carry out issuance and trading activities.

Engaging in the tokenization of real-world assets domestically, as well as providing related intermediary, information technology services, etc., which are suspected of illegal issuance of token vouchers, unauthorized public offering of securities, illegal operation of securities and futures business, illegal fundraising, and other illegal financial activities, shall be prohibited; except for relevant business activities carried out with the approval of the competent authorities in accordance with the law and regulations and relying on specific financial infrastructures. Overseas entities and individuals are not allowed to illegally provide services related to the tokenization of real-world assets to domestic entities in any form.

(III) Inter-agency Coordination. The People's Bank of China, together with the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Public Security, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the China Securities Regulatory Commission, the State Administration of Foreign Exchange, and other departments, will improve the work mechanism, strengthen coordination with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, coordinate efforts, and overall guide regions to carry out risk prevention and disposal of virtual currency-related illegal financial activities.

The China Securities Regulatory Commission, together with the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Public Security, the People's Bank of China, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the State Administration of Foreign Exchange, and other departments, will improve the work mechanism, strengthen coordination with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, coordinate efforts, and overall guide regions to carry out risk prevention and disposal of illegal financial activities related to the tokenization of real-world assets.

(IV) Strengthening Local Implementation. The people's governments at the provincial level are overall responsible for the prevention and disposal of risks related to virtual currencies and the tokenization of real-world assets in their respective administrative regions. The specific leading department is the local financial regulatory department, with participation from branches and dispatched institutions of the State Council's financial regulatory department, telecommunications regulators, public security, market supervision, and other departments, in coordination with cyberspace departments, courts, and procuratorates, to improve the normalization of the work mechanism, effectively connect with the relevant work mechanisms of central departments, form a cooperative and coordinated working pattern between central and local governments, effectively prevent and properly handle risks related to virtual currencies and the tokenization of real-world assets, and maintain economic and financial order and social stability.

(5) Enhanced Risk Monitoring. The People's Bank of China, China Securities Regulatory Commission, National Development and Reform Commission, Ministry of Industry and Information Technology, Ministry of Public Security, State Administration of Foreign Exchange, Cyberspace Administration of China, and other departments continue to improve monitoring techniques and system support, enhance cross-departmental data analysis and sharing, establish sound information sharing and cross-validation mechanisms, promptly grasp the risk situation of activities related to virtual currency and real-world asset tokenization. Local governments at all levels give full play to the role of local monitoring and early warning mechanisms. Local financial regulatory authorities, together with branches and agencies of the State Council's financial regulatory authorities, as well as departments of cyberspace and public security, ensure effective connection between online monitoring, offline investigation, and fund tracking, efficiently and accurately identify activities related to virtual currency and real-world asset tokenization, promptly share risk information, improve early warning information dissemination, verification, and rapid response mechanisms.

(6) Strengthened Oversight of Financial Institutions, Intermediaries, and Technology Service Providers. Financial institutions (including non-bank payment institutions) are prohibited from providing account opening, fund transfer, and clearing services for virtual currency-related business activities, issuing and selling financial products related to virtual currency, including virtual currency and related financial products in the scope of collateral, conducting insurance business related to virtual currency, or including virtual currency in the scope of insurance liability. Financial institutions (including non-bank payment institutions) are prohibited from providing custody, clearing, and settlement services for unauthorized real-world asset tokenization-related business and related financial products. Relevant intermediary institutions and information technology service providers are prohibited from providing intermediary, technical, or other services for unauthorized real-world asset tokenization-related businesses and related financial products.

(7) Enhanced Management of Internet Information Content and Access. Internet enterprises are prohibited from providing online business venues, commercial displays, marketing, advertising, or paid traffic diversion services for virtual currency and real-world asset tokenization-related business activities. Upon discovering clues of illegal activities, they should promptly report to relevant departments and provide technical support and assistance for related investigations and inquiries. Based on the clues transferred by the financial regulatory authorities, the cyberspace administration, telecommunications authorities, and public security departments should promptly close and deal with websites, mobile applications (including mini-programs), and public accounts engaged in virtual currency and real-world asset tokenization-related business activities in accordance with the law.

(8) Strengthened Entity Registration and Advertisement Management. Market supervision departments strengthen entity registration and management, and enterprise and individual business registrations must not contain terms such as "virtual currency," "virtual asset," "cryptocurrency," "crypto asset," "stablecoin," "real-world asset tokenization," or "RWA" in their names or business scopes. Market supervision departments, together with financial regulatory authorities, legally enhance the supervision of advertisements related to virtual currency and real-world asset tokenization, promptly investigating and handling relevant illegal advertisements.

(IX) Continued Rectification of Virtual Currency Mining Activities. The National Development and Reform Commission, together with relevant departments, strictly controls virtual currency mining activities, continuously promotes the rectification of virtual currency mining activities. The people's governments of various provinces take overall responsibility for the rectification of "mining" within their respective administrative regions. In accordance with the requirements of the National Development and Reform Commission and other departments in the "Notice on the Rectification of Virtual Currency Mining Activities" (NDRC Energy-saving Building [2021] No. 1283) and the provisions of the "Guidance Catalog for Industrial Structure Adjustment (2024 Edition)," a comprehensive review, investigation, and closure of existing virtual currency mining projects are conducted, new mining projects are strictly prohibited, and mining machine production enterprises are strictly prohibited from providing mining machine sales and other services within the country.

(X) Severe Crackdown on Related Illegal Financial Activities. Upon discovering clues to illegal financial activities related to virtual currency and the tokenization of real-world assets, local financial regulatory authorities, branches of the State Council's financial regulatory authorities, and other relevant departments promptly investigate, determine, and properly handle the issues in accordance with the law, and seriously hold the relevant entities and individuals legally responsible. Those suspected of crimes are transferred to the judicial authorities for processing according to the law.

(XI) Severe Crackdown on Related Illegal and Criminal Activities. The Ministry of Public Security, the People's Bank of China, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the China Securities Regulatory Commission, as well as judicial and procuratorial organs, in accordance with their respective responsibilities, rigorously crack down on illegal and criminal activities related to virtual currency, the tokenization of real-world assets, such as fraud, money laundering, illegal business operations, pyramid schemes, illegal fundraising, and other illegal and criminal activities carried out under the guise of virtual currency, the tokenization of real-world assets, etc.

(XII) Strengthen Industry Self-discipline. Relevant industry associations should enhance membership management and policy advocacy, based on their own responsibilities, advocate and urge member units to resist illegal financial activities related to virtual currency and the tokenization of real-world assets. Member units that violate regulatory policies and industry self-discipline rules are to be disciplined in accordance with relevant self-regulatory management regulations. By leveraging various industry infrastructure, conduct risk monitoring related to virtual currency, the tokenization of real-world assets, and promptly transfer issue clues to relevant departments.

(XIII) Without the approval of relevant departments in accordance with the law and regulations, domestic entities and foreign entities controlled by them may not issue virtual currency overseas.

(XIV) Domestic entities engaging directly or indirectly in overseas external debt-based tokenization of real-world assets, or conducting asset securitization activities abroad based on domestic ownership rights, income rights, etc. (hereinafter referred to as domestic equity), should be strictly regulated in accordance with the principles of "same business, same risk, same rules." The National Development and Reform Commission, the China Securities Regulatory Commission, the State Administration of Foreign Exchange, and other relevant departments regulate it according to their respective responsibilities. For other forms of overseas real-world asset tokenization activities based on domestic equity by domestic entities, the China Securities Regulatory Commission, together with relevant departments, supervise according to their division of responsibilities. Without the consent and filing of relevant departments, no unit or individual may engage in the above-mentioned business.

(15) Overseas subsidiaries and branches of domestic financial institutions providing Real World Asset Tokenization-related services overseas shall do so legally and prudently. They shall have professional personnel and systems in place to effectively mitigate business risks, strictly implement customer onboarding, suitability management, anti-money laundering requirements, and incorporate them into the domestic financial institutions' compliance and risk management system. Intermediaries and information technology service providers offering Real World Asset Tokenization services abroad based on domestic equity or conducting Real World Asset Tokenization business in the form of overseas debt for domestic entities directly or indirectly venturing abroad must strictly comply with relevant laws and regulations. They should establish and improve relevant compliance and internal control systems in accordance with relevant normative requirements, strengthen business and risk control, and report the business developments to the relevant regulatory authorities for approval or filing.

(16) Strengthen organizational leadership and overall coordination. All departments and regions should attach great importance to the prevention of risks related to virtual currencies and Real World Asset Tokenization, strengthen organizational leadership, clarify work responsibilities, form a long-term effective working mechanism with centralized coordination, local implementation, and shared responsibilities, maintain high pressure, dynamically monitor risks, effectively prevent and mitigate risks in an orderly and efficient manner, legally protect the property security of the people, and make every effort to maintain economic and financial order and social stability.

(17) Widely carry out publicity and education. All departments, regions, and industry associations should make full use of various media and other communication channels to disseminate information through legal and policy interpretation, analysis of typical cases, and education on investment risks, etc. They should promote the illegality and harm of virtual currencies and Real World Asset Tokenization-related businesses and their manifestations, fully alert to potential risks and hidden dangers, and enhance public awareness and identification capabilities for risk prevention.

(18) Engaging in illegal financial activities related to virtual currencies and Real World Asset Tokenization in violation of this notice, as well as providing services for virtual currencies and Real World Asset Tokenization-related businesses, shall be punished in accordance with relevant regulations. If it constitutes a crime, criminal liability shall be pursued according to the law. For domestic entities and individuals who knowingly or should have known that overseas entities illegally provided virtual currency or Real World Asset Tokenization-related services to domestic entities and still assisted them, relevant responsibilities shall be pursued according to the law. If it constitutes a crime, criminal liability shall be pursued according to the law.

(19) If any unit or individual invests in virtual currencies, Real World Asset Tokens, and related financial products against public order and good customs, the relevant civil legal actions shall be invalid, and any resulting losses shall be borne by them. If there are suspicions of disrupting financial order and jeopardizing financial security, the relevant departments shall deal with them according to the law.

This notice shall enter into force upon the date of its issuance. The People's Bank of China and ten other departments' "Notice on Further Preventing and Dealing with the Risks of Virtual Currency Trading Speculation" (Yinfa [2021] No. 237) is hereby repealed.

Former Partner's Perspective on Multicoin: Kyle's Exit, But the Game He Left Behind Just Getting Started

Why Bitcoin Is Falling Now: The Real Reasons Behind BTC's Crash & WEEX's Smart Profit Playbook

Bitcoin's ongoing crash explained: Discover the 5 hidden triggers behind BTC's plunge & how WEEX's Auto Earn and Trade to Earn strategies help traders profit from crypto market volatility.

Wall Street's Hottest Trades See Exodus

Vitalik Discusses Ethereum Scaling Path, Circle Announces Partnership with Polymarket, What's the Overseas Crypto Community Talking About Today?

Believing in the Capital Markets - The Essence and Core Value of Cryptocurrency

Polymarket's 'Weatherman': Predict Temperature, Win Million-Dollar Payout

$15K+ Profits: The 4 AI Trading Secrets WEEX Hackathon Prelim Winners Used to Dominate Volatile Crypto Markets

How WEEX Hackathon's top AI trading strategies made $15K+ in crypto markets: 4 proven rules for ETH/BTC trading, market structure analysis, and risk management in volatile conditions.

A nearly 20% one-day plunge, how long has it been since you last saw a $60,000 Bitcoin?

Raoul Pal: I've seen every single panic, and they are never the end.

Key Market Information Discrepancy on February 6th - A Must-Read! | Alpha Morning Report

2026 Crypto Industry's First Snowfall

The Harsh Reality Behind the $26 Billion Crypto Liquidation: Liquidity Is Killing the Market

Why Is Gold, US Stocks, Bitcoin All Falling?

Key Market Intelligence for February 5th, how much did you miss out on?

Wintermute: By 2026, crypto had gradually become the settlement layer of the Internet economy

Token Cannot Compound, Where Is the Real Investment Opportunity?

February 6th Market Key Intelligence, How Much Did You Miss?

China's Central Bank and Eight Other Departments' Latest Regulatory Focus: Key Attention to RWA Tokenized Asset Risk

Foreword: Today, the People's Bank of China's website published the "Notice of the People's Bank of China, National Development and Reform Commission, Ministry of Industry and Information Technology, Ministry of Public Security, State Administration for Market Regulation, China Banking and Insurance Regulatory Commission, China Securities Regulatory Commission, State Administration of Foreign Exchange on Further Preventing and Dealing with Risks Related to Virtual Currency and Others (Yinfa [2026] No. 42)", the latest regulatory requirements from the eight departments including the central bank, which are basically consistent with the regulatory requirements of recent years. The main focus of the regulation is on speculative activities such as virtual currency trading, exchanges, ICOs, overseas platform services, and this time, regulatory oversight of RWA has been added, explicitly prohibiting RWA tokenization, stablecoins (especially those pegged to the RMB). The following is the full text:

To the people's governments of all provinces, autonomous regions, and municipalities directly under the Central Government, the Xinjiang Production and Construction Corps:

Recently, there have been speculative activities related to virtual currency and Real-World Assets (RWA) tokenization, disrupting the economic and financial order and jeopardizing the property security of the people. In order to further prevent and address the risks related to virtual currency and Real-World Assets tokenization, effectively safeguard national security and social stability, in accordance with the "Law of the People's Republic of China on the People's Bank of China," "Law of the People's Republic of China on Commercial Banks," "Securities Law of the People's Republic of China," "Law of the People's Republic of China on Securities Investment Funds," "Law of the People's Republic of China on Futures and Derivatives," "Cybersecurity Law of the People's Republic of China," "Regulations of the People's Republic of China on the Administration of Renminbi," "Regulations on Prevention and Disposal of Illegal Fundraising," "Regulations of the People's Republic of China on Foreign Exchange Administration," "Telecommunications Regulations of the People's Republic of China," and other provisions, after reaching consensus with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, and with the approval of the State Council, the relevant matters are notified as follows:

(I) Virtual currency does not possess the legal status equivalent to fiat currency. Virtual currencies such as Bitcoin, Ether, Tether, etc., have the main characteristics of being issued by non-monetary authorities, using encryption technology and distributed ledger or similar technology, existing in digital form, etc. They do not have legal tender status, should not and cannot be circulated and used as currency in the market.

The business activities related to virtual currency are classified as illegal financial activities. The exchange of fiat currency and virtual currency within the territory, exchange of virtual currencies, acting as a central counterparty in buying and selling virtual currencies, providing information intermediary and pricing services for virtual currency transactions, token issuance financing, and trading of virtual currency-related financial products, etc., fall under illegal financial activities, such as suspected illegal issuance of token vouchers, unauthorized public issuance of securities, illegal operation of securities and futures business, illegal fundraising, etc., are strictly prohibited across the board and resolutely banned in accordance with the law. Overseas entities and individuals are not allowed to provide virtual currency-related services to domestic entities in any form.

A stablecoin pegged to a fiat currency indirectly fulfills some functions of the fiat currency in circulation. Without the consent of relevant authorities in accordance with the law and regulations, any domestic or foreign entity or individual is not allowed to issue a RMB-pegged stablecoin overseas.

(II)Tokenization of Real-World Assets refers to the use of encryption technology and distributed ledger or similar technologies to transform ownership rights, income rights, etc., of assets into tokens (tokens) or other interests or bond certificates with token (token) characteristics, and carry out issuance and trading activities.

Engaging in the tokenization of real-world assets domestically, as well as providing related intermediary, information technology services, etc., which are suspected of illegal issuance of token vouchers, unauthorized public offering of securities, illegal operation of securities and futures business, illegal fundraising, and other illegal financial activities, shall be prohibited; except for relevant business activities carried out with the approval of the competent authorities in accordance with the law and regulations and relying on specific financial infrastructures. Overseas entities and individuals are not allowed to illegally provide services related to the tokenization of real-world assets to domestic entities in any form.

(III) Inter-agency Coordination. The People's Bank of China, together with the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Public Security, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the China Securities Regulatory Commission, the State Administration of Foreign Exchange, and other departments, will improve the work mechanism, strengthen coordination with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, coordinate efforts, and overall guide regions to carry out risk prevention and disposal of virtual currency-related illegal financial activities.

The China Securities Regulatory Commission, together with the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Public Security, the People's Bank of China, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the State Administration of Foreign Exchange, and other departments, will improve the work mechanism, strengthen coordination with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, coordinate efforts, and overall guide regions to carry out risk prevention and disposal of illegal financial activities related to the tokenization of real-world assets.

(IV) Strengthening Local Implementation. The people's governments at the provincial level are overall responsible for the prevention and disposal of risks related to virtual currencies and the tokenization of real-world assets in their respective administrative regions. The specific leading department is the local financial regulatory department, with participation from branches and dispatched institutions of the State Council's financial regulatory department, telecommunications regulators, public security, market supervision, and other departments, in coordination with cyberspace departments, courts, and procuratorates, to improve the normalization of the work mechanism, effectively connect with the relevant work mechanisms of central departments, form a cooperative and coordinated working pattern between central and local governments, effectively prevent and properly handle risks related to virtual currencies and the tokenization of real-world assets, and maintain economic and financial order and social stability.

(5) Enhanced Risk Monitoring. The People's Bank of China, China Securities Regulatory Commission, National Development and Reform Commission, Ministry of Industry and Information Technology, Ministry of Public Security, State Administration of Foreign Exchange, Cyberspace Administration of China, and other departments continue to improve monitoring techniques and system support, enhance cross-departmental data analysis and sharing, establish sound information sharing and cross-validation mechanisms, promptly grasp the risk situation of activities related to virtual currency and real-world asset tokenization. Local governments at all levels give full play to the role of local monitoring and early warning mechanisms. Local financial regulatory authorities, together with branches and agencies of the State Council's financial regulatory authorities, as well as departments of cyberspace and public security, ensure effective connection between online monitoring, offline investigation, and fund tracking, efficiently and accurately identify activities related to virtual currency and real-world asset tokenization, promptly share risk information, improve early warning information dissemination, verification, and rapid response mechanisms.

(6) Strengthened Oversight of Financial Institutions, Intermediaries, and Technology Service Providers. Financial institutions (including non-bank payment institutions) are prohibited from providing account opening, fund transfer, and clearing services for virtual currency-related business activities, issuing and selling financial products related to virtual currency, including virtual currency and related financial products in the scope of collateral, conducting insurance business related to virtual currency, or including virtual currency in the scope of insurance liability. Financial institutions (including non-bank payment institutions) are prohibited from providing custody, clearing, and settlement services for unauthorized real-world asset tokenization-related business and related financial products. Relevant intermediary institutions and information technology service providers are prohibited from providing intermediary, technical, or other services for unauthorized real-world asset tokenization-related businesses and related financial products.

(7) Enhanced Management of Internet Information Content and Access. Internet enterprises are prohibited from providing online business venues, commercial displays, marketing, advertising, or paid traffic diversion services for virtual currency and real-world asset tokenization-related business activities. Upon discovering clues of illegal activities, they should promptly report to relevant departments and provide technical support and assistance for related investigations and inquiries. Based on the clues transferred by the financial regulatory authorities, the cyberspace administration, telecommunications authorities, and public security departments should promptly close and deal with websites, mobile applications (including mini-programs), and public accounts engaged in virtual currency and real-world asset tokenization-related business activities in accordance with the law.

(8) Strengthened Entity Registration and Advertisement Management. Market supervision departments strengthen entity registration and management, and enterprise and individual business registrations must not contain terms such as "virtual currency," "virtual asset," "cryptocurrency," "crypto asset," "stablecoin," "real-world asset tokenization," or "RWA" in their names or business scopes. Market supervision departments, together with financial regulatory authorities, legally enhance the supervision of advertisements related to virtual currency and real-world asset tokenization, promptly investigating and handling relevant illegal advertisements.

(IX) Continued Rectification of Virtual Currency Mining Activities. The National Development and Reform Commission, together with relevant departments, strictly controls virtual currency mining activities, continuously promotes the rectification of virtual currency mining activities. The people's governments of various provinces take overall responsibility for the rectification of "mining" within their respective administrative regions. In accordance with the requirements of the National Development and Reform Commission and other departments in the "Notice on the Rectification of Virtual Currency Mining Activities" (NDRC Energy-saving Building [2021] No. 1283) and the provisions of the "Guidance Catalog for Industrial Structure Adjustment (2024 Edition)," a comprehensive review, investigation, and closure of existing virtual currency mining projects are conducted, new mining projects are strictly prohibited, and mining machine production enterprises are strictly prohibited from providing mining machine sales and other services within the country.

(X) Severe Crackdown on Related Illegal Financial Activities. Upon discovering clues to illegal financial activities related to virtual currency and the tokenization of real-world assets, local financial regulatory authorities, branches of the State Council's financial regulatory authorities, and other relevant departments promptly investigate, determine, and properly handle the issues in accordance with the law, and seriously hold the relevant entities and individuals legally responsible. Those suspected of crimes are transferred to the judicial authorities for processing according to the law.

(XI) Severe Crackdown on Related Illegal and Criminal Activities. The Ministry of Public Security, the People's Bank of China, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the China Securities Regulatory Commission, as well as judicial and procuratorial organs, in accordance with their respective responsibilities, rigorously crack down on illegal and criminal activities related to virtual currency, the tokenization of real-world assets, such as fraud, money laundering, illegal business operations, pyramid schemes, illegal fundraising, and other illegal and criminal activities carried out under the guise of virtual currency, the tokenization of real-world assets, etc.

(XII) Strengthen Industry Self-discipline. Relevant industry associations should enhance membership management and policy advocacy, based on their own responsibilities, advocate and urge member units to resist illegal financial activities related to virtual currency and the tokenization of real-world assets. Member units that violate regulatory policies and industry self-discipline rules are to be disciplined in accordance with relevant self-regulatory management regulations. By leveraging various industry infrastructure, conduct risk monitoring related to virtual currency, the tokenization of real-world assets, and promptly transfer issue clues to relevant departments.

(XIII) Without the approval of relevant departments in accordance with the law and regulations, domestic entities and foreign entities controlled by them may not issue virtual currency overseas.

(XIV) Domestic entities engaging directly or indirectly in overseas external debt-based tokenization of real-world assets, or conducting asset securitization activities abroad based on domestic ownership rights, income rights, etc. (hereinafter referred to as domestic equity), should be strictly regulated in accordance with the principles of "same business, same risk, same rules." The National Development and Reform Commission, the China Securities Regulatory Commission, the State Administration of Foreign Exchange, and other relevant departments regulate it according to their respective responsibilities. For other forms of overseas real-world asset tokenization activities based on domestic equity by domestic entities, the China Securities Regulatory Commission, together with relevant departments, supervise according to their division of responsibilities. Without the consent and filing of relevant departments, no unit or individual may engage in the above-mentioned business.

(15) Overseas subsidiaries and branches of domestic financial institutions providing Real World Asset Tokenization-related services overseas shall do so legally and prudently. They shall have professional personnel and systems in place to effectively mitigate business risks, strictly implement customer onboarding, suitability management, anti-money laundering requirements, and incorporate them into the domestic financial institutions' compliance and risk management system. Intermediaries and information technology service providers offering Real World Asset Tokenization services abroad based on domestic equity or conducting Real World Asset Tokenization business in the form of overseas debt for domestic entities directly or indirectly venturing abroad must strictly comply with relevant laws and regulations. They should establish and improve relevant compliance and internal control systems in accordance with relevant normative requirements, strengthen business and risk control, and report the business developments to the relevant regulatory authorities for approval or filing.

(16) Strengthen organizational leadership and overall coordination. All departments and regions should attach great importance to the prevention of risks related to virtual currencies and Real World Asset Tokenization, strengthen organizational leadership, clarify work responsibilities, form a long-term effective working mechanism with centralized coordination, local implementation, and shared responsibilities, maintain high pressure, dynamically monitor risks, effectively prevent and mitigate risks in an orderly and efficient manner, legally protect the property security of the people, and make every effort to maintain economic and financial order and social stability.

(17) Widely carry out publicity and education. All departments, regions, and industry associations should make full use of various media and other communication channels to disseminate information through legal and policy interpretation, analysis of typical cases, and education on investment risks, etc. They should promote the illegality and harm of virtual currencies and Real World Asset Tokenization-related businesses and their manifestations, fully alert to potential risks and hidden dangers, and enhance public awareness and identification capabilities for risk prevention.

(18) Engaging in illegal financial activities related to virtual currencies and Real World Asset Tokenization in violation of this notice, as well as providing services for virtual currencies and Real World Asset Tokenization-related businesses, shall be punished in accordance with relevant regulations. If it constitutes a crime, criminal liability shall be pursued according to the law. For domestic entities and individuals who knowingly or should have known that overseas entities illegally provided virtual currency or Real World Asset Tokenization-related services to domestic entities and still assisted them, relevant responsibilities shall be pursued according to the law. If it constitutes a crime, criminal liability shall be pursued according to the law.

(19) If any unit or individual invests in virtual currencies, Real World Asset Tokens, and related financial products against public order and good customs, the relevant civil legal actions shall be invalid, and any resulting losses shall be borne by them. If there are suspicions of disrupting financial order and jeopardizing financial security, the relevant departments shall deal with them according to the law.

This notice shall enter into force upon the date of its issuance. The People's Bank of China and ten other departments' "Notice on Further Preventing and Dealing with the Risks of Virtual Currency Trading Speculation" (Yinfa [2021] No. 237) is hereby repealed.

Former Partner's Perspective on Multicoin: Kyle's Exit, But the Game He Left Behind Just Getting Started

Why Bitcoin Is Falling Now: The Real Reasons Behind BTC's Crash & WEEX's Smart Profit Playbook

Bitcoin's ongoing crash explained: Discover the 5 hidden triggers behind BTC's plunge & how WEEX's Auto Earn and Trade to Earn strategies help traders profit from crypto market volatility.